Purchasing a home is one of the most significant financial decisions you will ever make, and for many people, it requires taking out a mortgage loan. A mortgage allows you to borrow money from a lender to buy a property, which you will repay over time with interest. However, qualifying for a mortgage can be a challenging process that requires careful planning and an understanding of what lenders are looking for.

In this article, we will explore the steps you need to take to qualify for a mortgage, the factors that influence your eligibility, and tips for improving your chances of approval.

What Is a Mortgage?

A mortgage is a loan used to purchase a home or other real estate. In exchange for lending you the money to buy the property, the lender places a lien on the home, meaning the property serves as collateral. If you fail to repay the mortgage, the lender has the legal right to foreclose on the property and sell it to recover the outstanding debt.

Mortgages typically come with long repayment terms, usually 15 to 30 years, and feature both principal (the original amount borrowed) and interest payments. The interest rate and loan type (e.g., fixed-rate, adjustable-rate) will vary depending on several factors.

What Lenders Look for in Mortgage Applicants

Lenders evaluate multiple factors when deciding whether to approve a mortgage application. The goal is to assess your ability to repay the loan over time and ensure that you are financially responsible. There are several key elements lenders consider when reviewing mortgage applications:

- Credit Score

- What It Is: Your credit score is a numerical representation of your creditworthiness, typically ranging from 300 to 850. It reflects how well you’ve managed debt in the past and helps lenders gauge the risk involved in lending to you.

- Why It Matters: A higher credit score indicates that you are a lower-risk borrower, which can lead to better loan terms, including a lower interest rate. Most lenders require a credit score of at least 620 for conventional loans, but a score of 740 or higher is ideal for securing the best interest rates.

- Income and Employment

- What It Is: Lenders will review your income and employment history to ensure you have a stable source of income to make mortgage payments.

- Why It Matters: Lenders want to be sure that you can afford your monthly mortgage payments. Typically, your monthly housing expenses (including the mortgage, property taxes, and insurance) should not exceed 28-31% of your gross monthly income. Additionally, lenders often look for a steady employment history, with at least two years of consistent work in the same field or industry.

- Debt-to-Income (DTI) Ratio

- What It Is: The debt-to-income ratio is a measure of your monthly debt payments compared to your monthly gross income. It is calculated by dividing your total monthly debt payments (including credit cards, student loans, car loans, etc.) by your gross monthly income.

- Why It Matters: A lower DTI ratio indicates that you have enough income to handle additional debt. Lenders generally look for a DTI ratio of 36% or lower, although some may allow up to 43% or higher, depending on the type of loan and the lender.

- Down Payment

- What It Is: A down payment is the amount of money you pay upfront toward the purchase of the home. It is typically expressed as a percentage of the home’s purchase price.

- Why It Matters: A larger down payment reduces the lender’s risk by decreasing the loan-to-value (LTV) ratio. In general, a down payment of at least 20% is recommended to avoid paying for private mortgage insurance (PMI). However, there are loan programs that allow smaller down payments, such as FHA loans (which require as little as 3.5% down) and VA loans (which may require no down payment).

- Assets and Savings

- What It Is: Lenders will want to know about your financial assets and savings to ensure that you have enough money to cover the down payment, closing costs, and any emergency expenses that may arise after you buy the home.

- Why It Matters: Having sufficient savings demonstrates financial responsibility and assures lenders that you have the ability to weather unexpected financial challenges. Lenders may require proof of your savings, such as bank statements, and may want to see that you have enough money to cover at least two to three months’ worth of mortgage payments after you buy the home.

- Property Appraisal

- What It Is: The lender will order a property appraisal to determine the market value of the home you wish to purchase. This helps the lender ensure that the property is worth the amount you’re borrowing.

- Why It Matters: If the property is appraised for less than the purchase price, the lender may not approve the full loan amount or may require a larger down payment to make up for the difference. Ensuring the home appraises for a reasonable amount is critical to securing a mortgage.

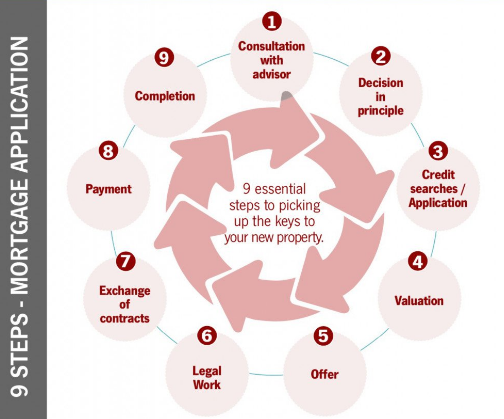

Steps to Qualify for a Mortgage

Now that you understand the key factors lenders consider, let’s walk through the steps you can take to qualify for a mortgage.

1. Check Your Credit Report and Score

Before applying for a mortgage, it’s essential to check your credit report and score. You can obtain a free copy of your credit report from each of the three major credit bureaus—Equifax, Experian, and TransUnion—once a year. Review the report for any errors or inaccuracies and dispute them if necessary. If your credit score is low, consider taking steps to improve it by paying off outstanding debts or reducing credit card balances.

2. Save for a Down Payment

A significant down payment will not only increase your chances of qualifying for a mortgage, but it will also help you secure better loan terms. Start saving early and explore ways to reduce expenses to accelerate your savings. If you’re a first-time homebuyer, look into loan programs that offer lower down payment options.

3. Determine Your Budget

Consider how much you can afford to borrow without overstretching your finances. Use an online mortgage calculator to estimate your monthly payments based on different loan amounts, interest rates, and loan terms. Factor in other homeownership costs, such as property taxes, homeowner’s insurance, and maintenance.

4. Gather Documentation

Lenders will require various documents to assess your financial situation. These may include:

- Proof of income (pay stubs, tax returns, W-2s)

- Proof of employment (offer letter or recent pay stubs)

- Bank statements and proof of savings

- Documentation of outstanding debts

- Tax returns from the past 2-3 years Gather all necessary paperwork in advance to streamline the application process.

5. Apply for a Mortgage Pre-Approval

A pre-approval is an indication from a lender that you qualify for a mortgage loan based on your financial profile. It’s a good idea to get pre-approved before you start house-hunting, as it shows sellers that you are a serious buyer and can afford the home. Pre-approval also helps you set a budget for your home search.

6. Shop Around for the Best Rates

Not all lenders offer the same rates or terms, so it’s essential to shop around. Compare mortgage offers from different banks, credit unions, and online lenders to find the best deal. Don’t forget to factor in the interest rate, loan term, and any fees or closing costs.

7. Work with a Real Estate Agent

Once you have your pre-approval in hand, it’s time to start looking for a home. Working with a real estate agent can help you navigate the home-buying process, negotiate prices, and ensure that you find a home that fits your budget.

8. Make an Offer and Finalize the Loan

When you’ve found the home you want to buy, make an offer. Once the offer is accepted, the lender will finalize the mortgage process. This includes ordering an appraisal, conducting a title search, and completing all necessary paperwork. If everything checks out, the lender will issue a final loan approval, and you’ll be ready to close on your new home.

Conclusion

Qualifying for a mortgage can seem like a complex process, but with careful preparation and attention to detail, you can increase your chances of approval. By focusing on your credit score, maintaining a stable income, saving for a down payment, and gathering the necessary documentation, you’ll be in a strong position to qualify for a mortgage. Shopping around for the best rates and loan terms can also save you money in the long run.

Remember that the key to qualifying for a mortgage is demonstrating your ability to repay the loan responsibly. By understanding what lenders look for and taking proactive steps to strengthen your financial profile, you’ll be on the path to homeownership in no time.

Leave a Reply